9 Thoughts on Meet the Club Board

Or the meeting with next to no new news

A couple of weeks ago the club announced a Meet the Board.

Out of nowhere, according to some. A belated response to (fabricated) rumours, according to others.

Whichever version you prefer, this was always going to be a serious meeting at a serious moment. Which means fewer jokes than usual.

For that, we apologise in advance. Normal service will resume shortly.

There was a time when Meet the Board events felt like theatre. Immersive theatre. Like the disaster experience in 2019.

Wednesday night wasn’t that.

This was a grown-up meeting. Questions were answered. Difficult topics weren’t smoothed over. The Club Board continued to step up and take their responsibility seriously. All of them, from the DT representatives, to the minority investors, not forgetting the NEDs, and finally the Chair.

Which will come as a disappointment to anyone who had already packed an emotional go-bag for administration, liquidation, or a surprise investor emerging from behind the south stand.

Here’s what actually happened.

Four things we already knew

1. The losses.

£600k down last year.

Record turnover. Wembley income. Commercial revenue at £1.1m. Hospitality running at around 80 percent of capacity.

And still, unmistakably, red ink.

This was the number everything else orbited. Not always explicitly, but constantly. Every potential decision discussed on makes more sense when you keep that figure in your head. It is the gravity beneath the conversation, pulling every topic slightly off its ideal path.

Context helps, at least emotionally. The average League One club loses around £5m a year.

In that sense, AFC Wimbledon is performing like a financial ascetic in a league of serial arsonists.

But that context doesn’t make the deficit disappear. We are still losing money. Not catastrophically. Not recklessly. But consistently. And that reality framed the entire evening, whether people wanted it to or not.

2. Cash flow tightens in mid-2026.

This is not a revelation and makes sense given the losses.

It has been explained repeatedly, in meetings, statements, and presentations, often by the same people patiently finding new ways to say the same thing.

Bond refinancing. Investor conversations. Revenue growth strategies. All of it points to the same pressure point in the calendar.

It is known. It is being managed.

It is not a secret cliff edge uncovered last week by someone on Facebook who “heard something on a podcast”

3. Michele Little is extremely good at refinancing bonds.

At this point she could probably do it while answering emails and stirring a cup of tea.

The Plough Lane Bond survey came back with reassuring numbers. Not perfect. But workable.

A little under 40 percent want repayment. Just over half are happy to roll over. A small but meaningful minority are willing to gift or convert to equity.

Better than last year. Better than expected.

The plan is straightforward. Reopen PLB to cover the £1.2m repayment requirement, then use any surplus to reduce higher-interest debt. Lower rates. Less bleeding.

It’s not exciting. But it is the kind of quiet competence that keeps clubs alive.

4. Investor conversations are ongoing.

Graeme Price laid out the process clearly. Initial contact handled carefully. Anything meaningful comes back to members.

Angus Fox spoke about one particular group with genuine enthusiasm. Meetings have taken place. Values discussed. Skills explored.

There are no names. No numbers. No deadlines. But there are NDAs.

That’s frustrating, especially for a fanbase who increasingly expect instant updates. But it is also exactly how serious investment conversations work. Anyone promising more than that at this stage probably isn’t worth listening to.

Two things we didn’t know

1. 50+1 is back. Now.

Well, we all knew the vote was coming back.

What we didn’t know was when.

Now we do.

The proposal to allow investment while retaining fan ownership above 50 percent is returning, and it is being bundled with constitutional changes. Because apparently the DTB has decided that if something is going to be difficult, it might as well be maximally difficult.

Last time, the vote was messy. Some members treated it as a referendum on individuals rather than the structure itself. A strategic decision got tangled up in personalities, tone, trust, and grievance. That helped nobody and clarified nothing.

This time feels different. Not calmer. More urgent.

The financial picture is clearer. The options are narrower. The runway is visibly shorter. The idea that we can simply wait another year and revisit this later feels increasingly fictional.

Bundling it with the constitution makes the choice harder, not easier. If you broadly support removing the 15 percent cap to make 50+1 workable, but disagree with specific elements of the new constitution, what are you supposed to do? Hold your nose? Walk away? Vote against something you largely support because you object to the packaging?

That awkwardness is not deliberate. It is the direct consequence of the previous vote failing. Delay always has a cost. This is part of it.

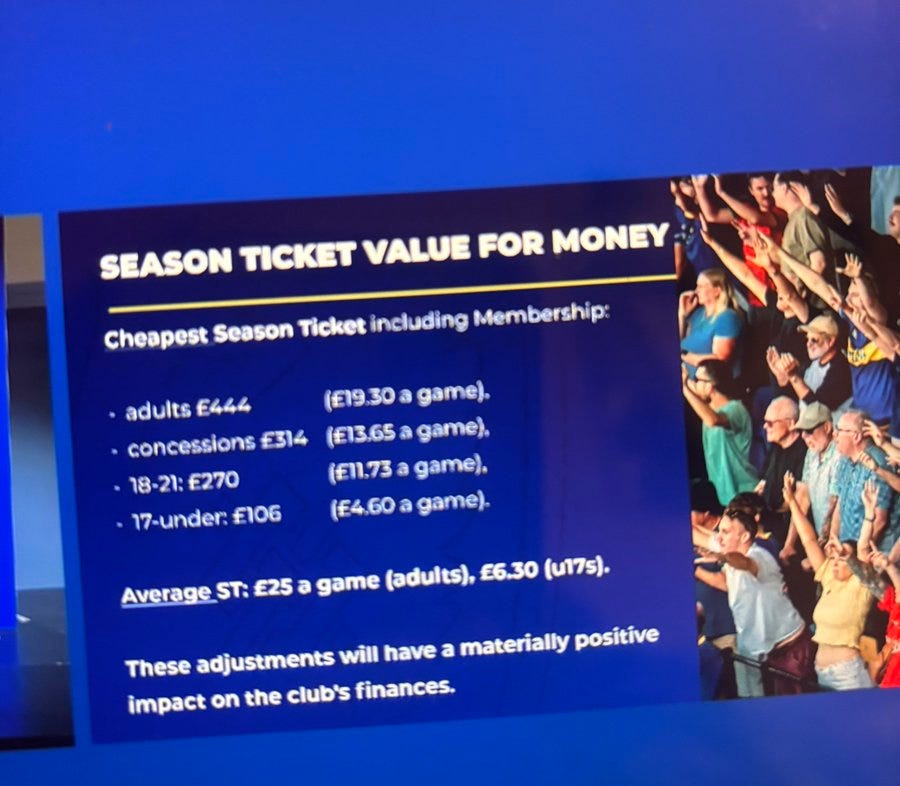

2. Season ticket prices. Up 13 percent.

This one lands hardest in the wallet.

A 13 percent increase is not abstract. It’s not theoretical. It hurts. Especially when your weekly shop already feels like a personal insult and everything else in life has crept up.

The obvious question was asked.

Does this depend on what league we’re in?

The answer was blunt.

“No.”

Ticketing accounts for roughly 30 percent of club income. That is the simple reality. James Woodroof described it as “difficult choices,” which is both accurate and unsatisfying.

It doesn’t make it easier to swallow. But it does explain why it’s happening.

Two things we still don’t know

1. What the regulator actually does for a club like AFC Wimbledon.

Angus was in Parliament last week. Met with the football regulator. Spoke up for fan-owned clubs. Secured a follow-up meeting.

All positive signals.

But “regulator ready” is a slogan, not a plan.

Still unclear.

2. What happens if the 50+1 vote fails again.

Nobody said it out loud on Tuesday night.

Nobody wants to. But it matters.

If the vote doesn’t pass, what then? Is there a Plan B? Or does even asking that question undermine the campaign itself?

The board’s position is consistent. Investment is needed. Fan ownership above 50 percent must be protected. The vote is the mechanism.

But mechanisms fail sometimes. And no one has explained what happens if this one does. Can we survive with our 75+1 model.

Graham said, “voting rights below 75% doesn’t end businesses, lack of cash flow does.”

One final thing.

The Rumours

In the weeks before this meeting, you could have been forgiven for thinking AFC Wimbledon was circling the drain. Administration was mentioned. Takeovers were speculated. The vibes were, to use a technical term, not good.

Some of that was background noise. Social media anxiety spirals. Facebook doom loops. Discord speculation.

But some of it felt more intentional.

Rumours directly leaked to podcasts. Framing designed to generate heat rather than light.

Who spoke? And why? We still don’t know.

There was a time when AFC Wimbledon podcasts positioned themselves as the sensible alternative to fan hysteria. The calm voices. The grown-ups. The ones who checked before they broadcast.

That feels less true at the moment. Rumour presented as journalism just makes everything worse.

Speculation dressed up as concern helps no one.

The board is trying to communicate. Slowly. Imperfectly. Repeatedly.

That job becomes much harder when half the audience has already decided the club is finished before the meeting even starts.

Closing thoughts

This was a pragmatic meeting about difficult realities.

We need more money than we currently generate. That hasn’t changed.

The routes forward are clear enough. Revenue growth. Investor partnerships. Bond refinancing. Eventually, stadium expansion.

What felt different on Tuesday was the tone. Honest without hysteria. Direct without overpromising.

Fan ownership above 50 percent matters.

Cash flow and financial realties also matter.

The next few months will test whether we can hold both ideas in our heads at the same time.

Until then, stay calm.

And maybe wait for the facts before sounding the alarm.

WombleWorld

Craig Cope finished the meeting with some budget left over. First time for everything. WW sources suggest he will be investing in WW+ membership for the whole playing squad